UI / UX Design

Loan Review Dashboard - designing the compliance workspace for consumer lending platforms

A compliance review dashboard consolidating identity, credit, fraud, and AML signals into one structured workspace that is designed for loan officers at regulated fintech lending platforms.

Year :

2023

Industry :

Fintech

Company

Compliance Innovation

Project Duration :

4 Months

OverView

Loan officers at consumer lending platforms make dozens of approve or reject decisions every day. Behind each decision is a completed application with outputs from identity verification, credit bureau, income verification, AML screening, and device fraud detection - separate systems, different formats, different compliance implications.

The real risk is not inefficiency. It is a missed fraud signal. On an unsecured personal loan, there is no collateral. A wrong approval is a written-off loan.

This project was to design the compliance review workspace from the ground up. A white-label platform lending companies deploy under their own brand, built to surface every verification signal in one structured interface, with actions tied directly to what triggered them, and a documented record of every decision made.

Outcome

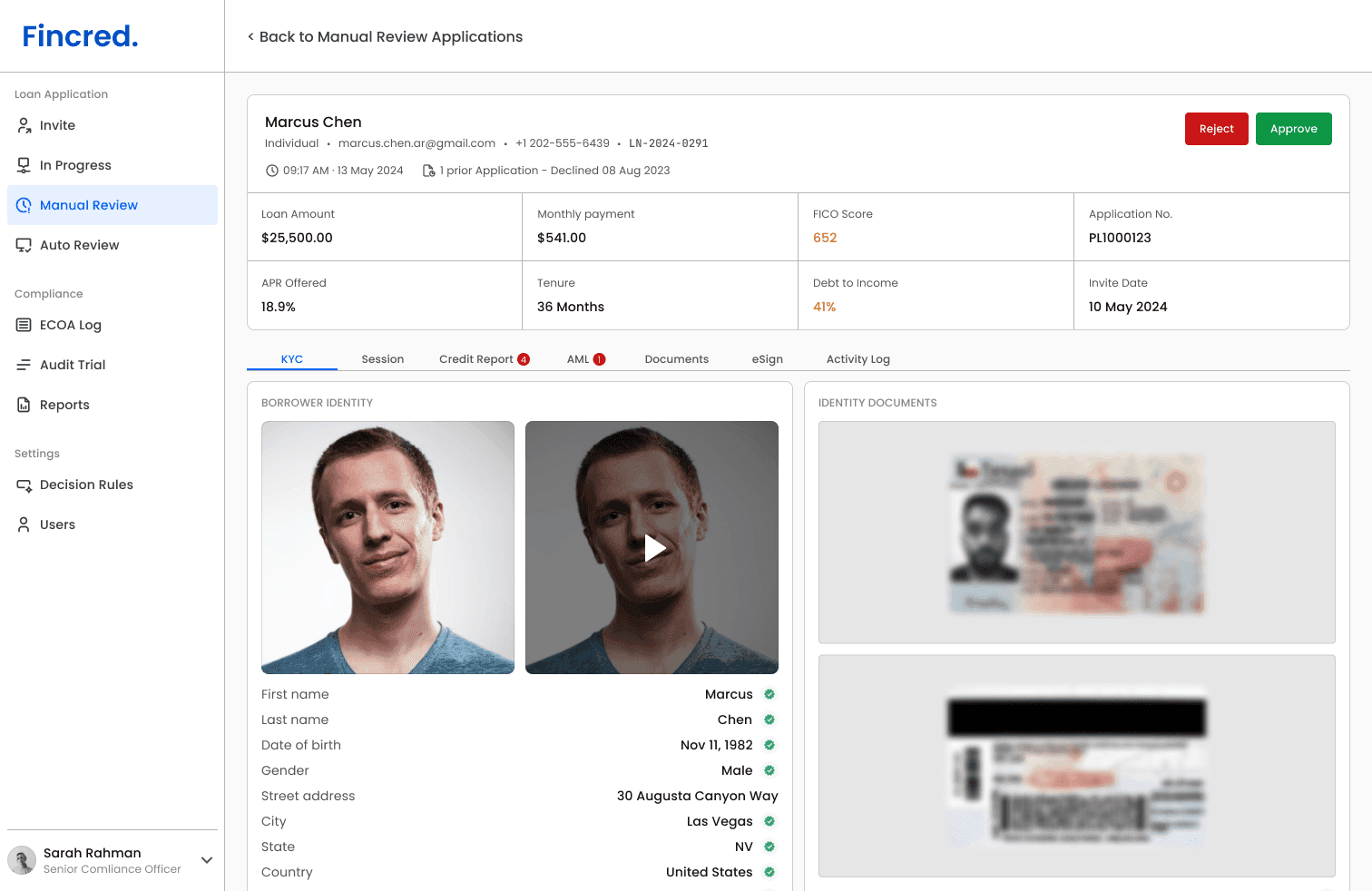

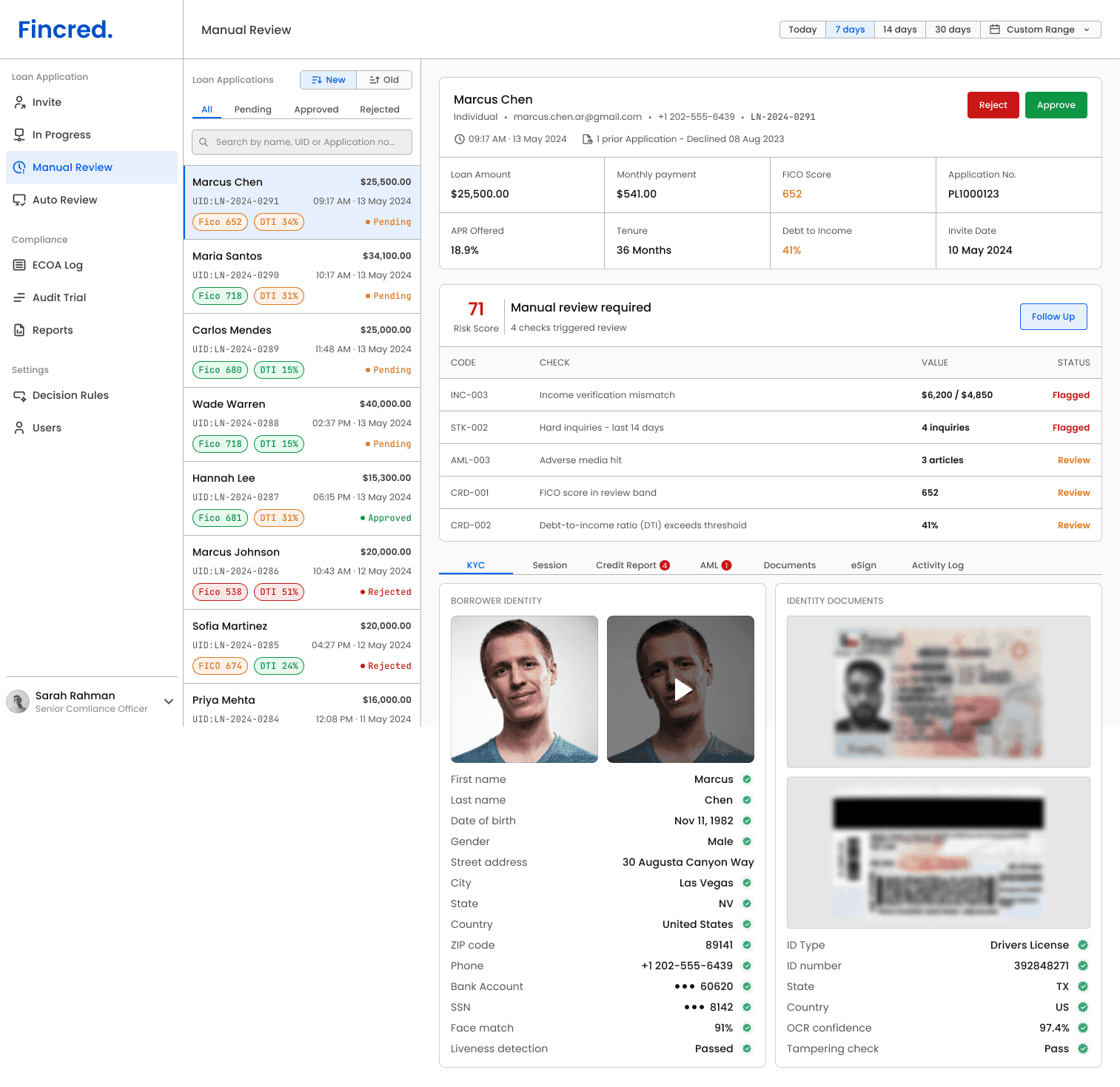

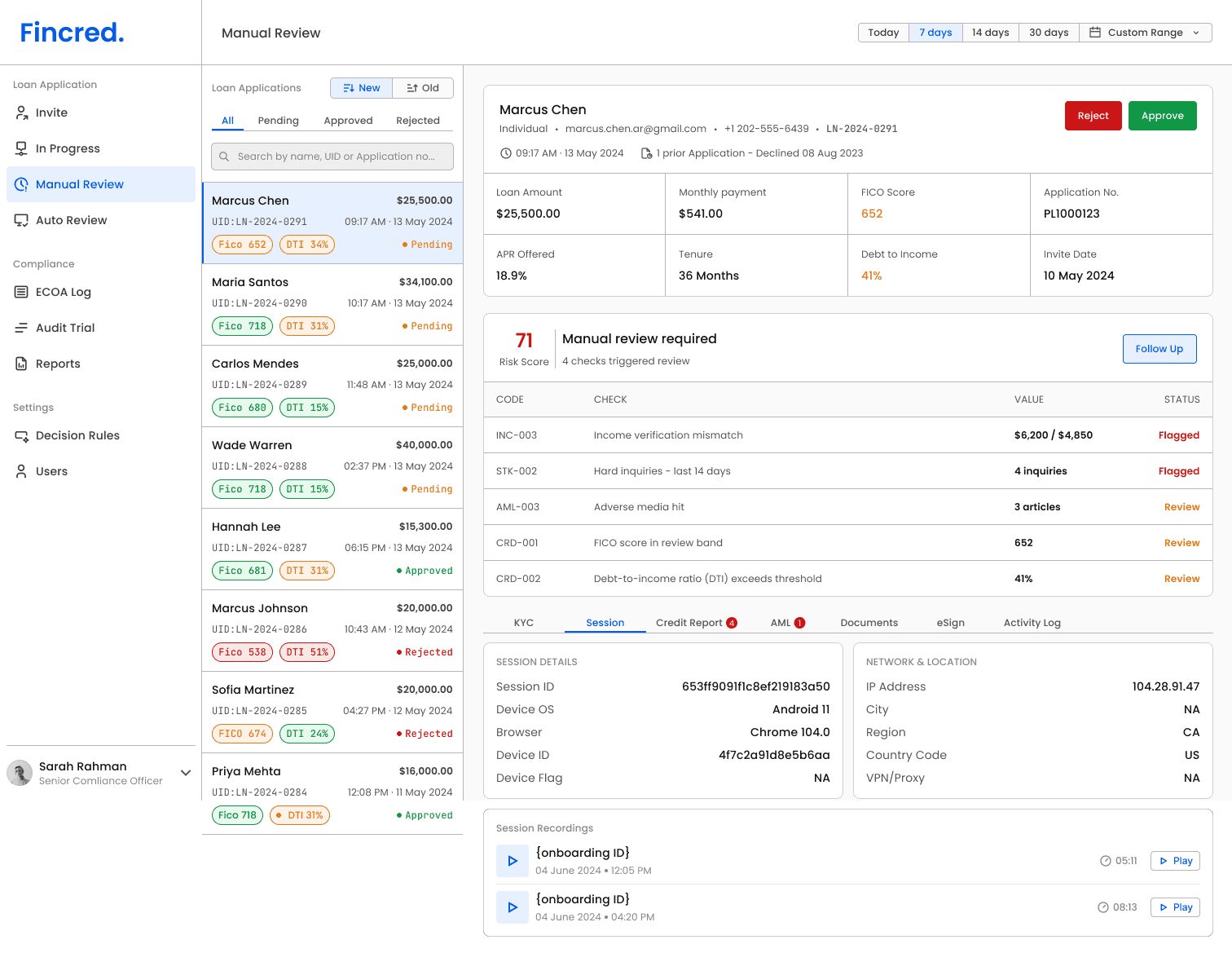

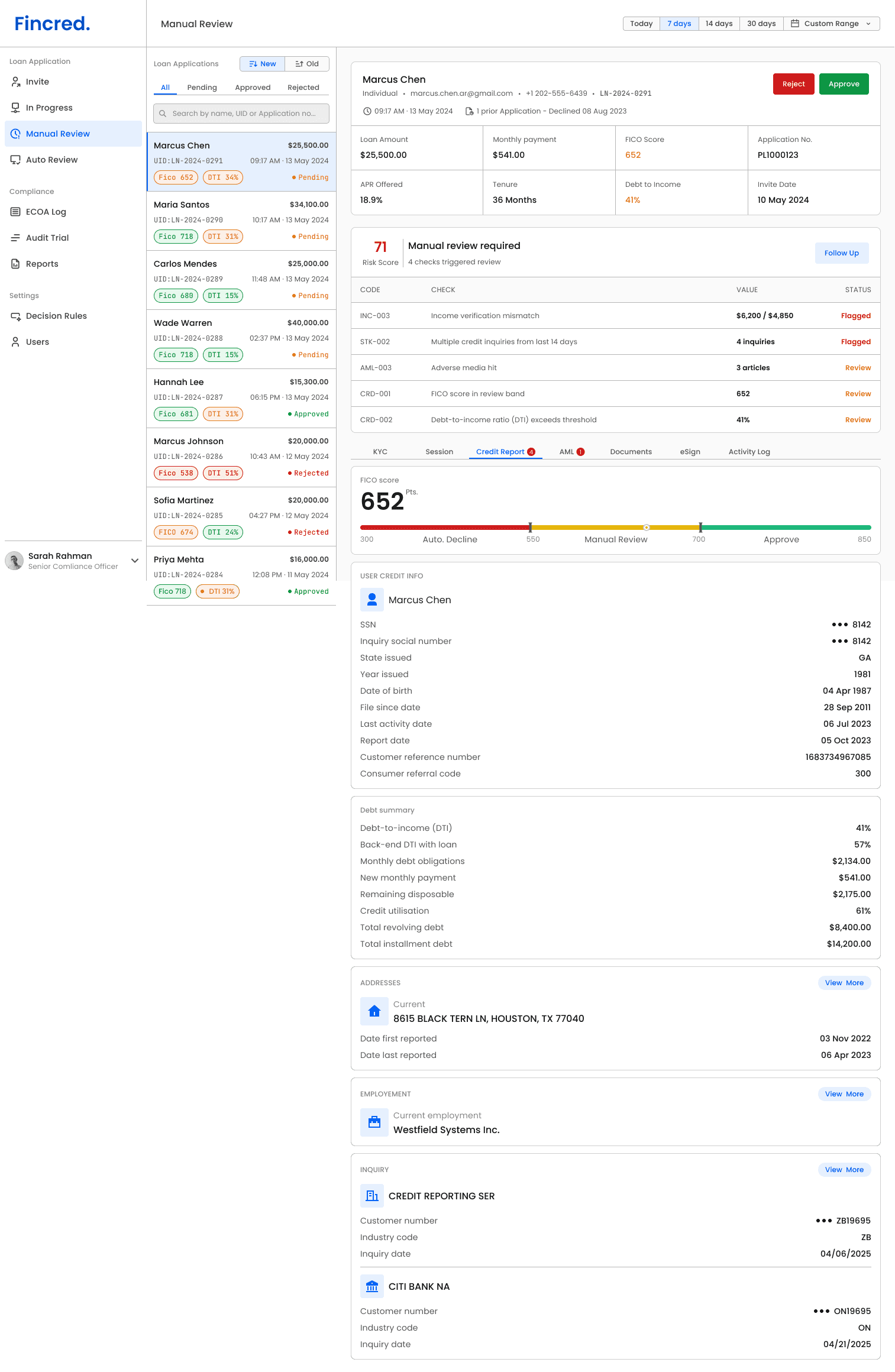

Designed a compliance review workspace that gives loan officers complete visibility into every verification signal - identity, credit report, income, fraud, and AML, in a single structured interface. An officer can move from application received to decision made without leaving the screen or switching tools.

Fraud signals that previously required manual cross-referencing across systems are now surfaced at the point of review, tied directly to the action needed to resolve them. A wrong approval on an unsecured personal loan has no recovery path. The design makes the right call harder to miss.

My Role

End-to-end product design, user research, information architecture, interaction design, and final UI. Collaborated with the product team on compliance requirements and lending workflow validation.

Problem

Every signal is there. The system to act on them isn't.

Loan officers need to make accurate credit decisions at speed but the data required to make that decision is spread across identity, credit, income, fraud, and AML systems with no unified view and no hierarchy telling them what matters most.

Fragmented verification data increases cognitive load at the exact moment it needs to be lowest. An officer processing disconnected signals manually is more likely to miss the connection between them. And on an unsecured loan, a missed fraud signal has no recovery path.

Not every flagged application is a rejection. Many are recoverable with one document or one clarification. Without a structured follow-up workflow, those borrowers are lost not because of the risk they posed but because the process had no way to bring them back.

Solution

Iteration 1

The first version was the obvious one. Every verification output in one place, identity, credit, income, fraud, AML, unified in a single interface. Technically complete. A loan officer could see everything without switching tools.

Final Design

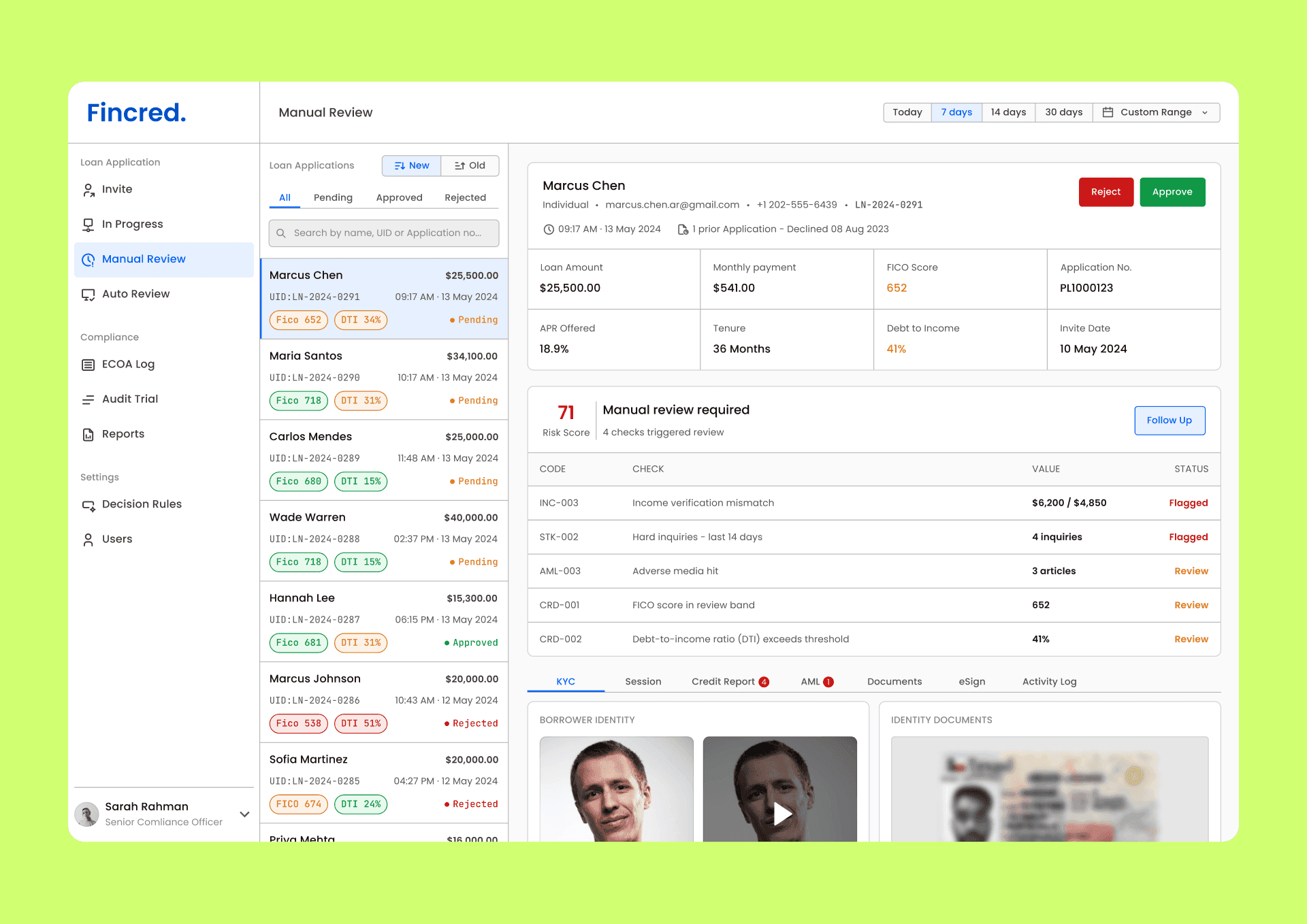

But seeing everything is not the same as knowing what matters. The officer was still doing the interpretive work manually, scanning a full list to find the three signals worth acting on. The interface had consolidated the data. It had not supported the decision.

That forced the real design question. An officer reviewing a loan application is not reading a report. They are looking for a pattern, a signal that one check alone might not confirm but two or three together do. The interface needed to reflect that. Surface what requires attention. Let the officer investigate the rest if they choose.

That shift changed the structure of the entire product. The review area became focused on triggered signals only. Full verification data remained accessible but was no longer the primary view. The officer lands on what matters, not on what exists.

Follow up with borrower feature

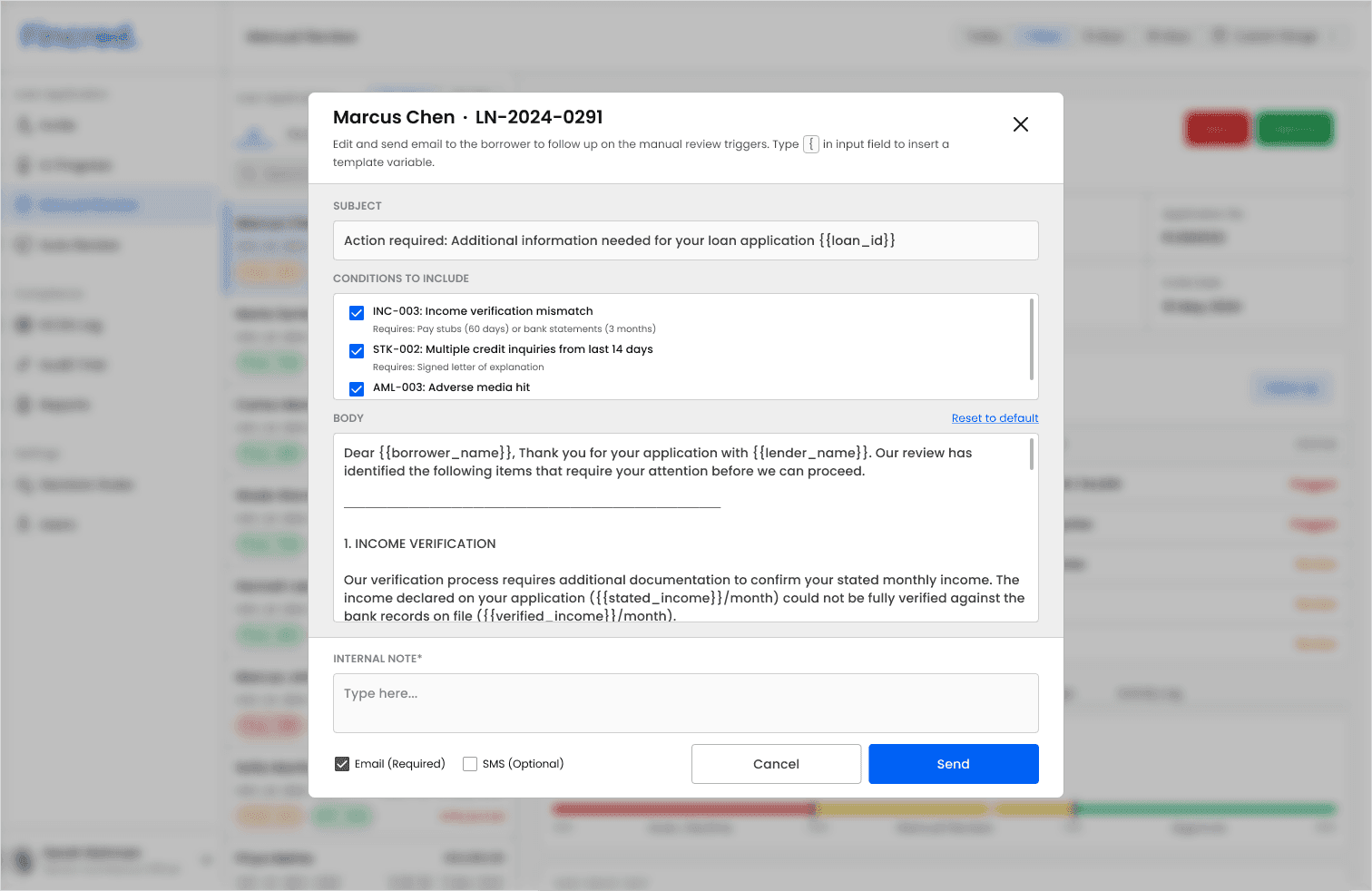

Not every flagged application is a rejection. Many just need one document or one clarification from the borrower. Without a structured way to ask, those applications quietly die.

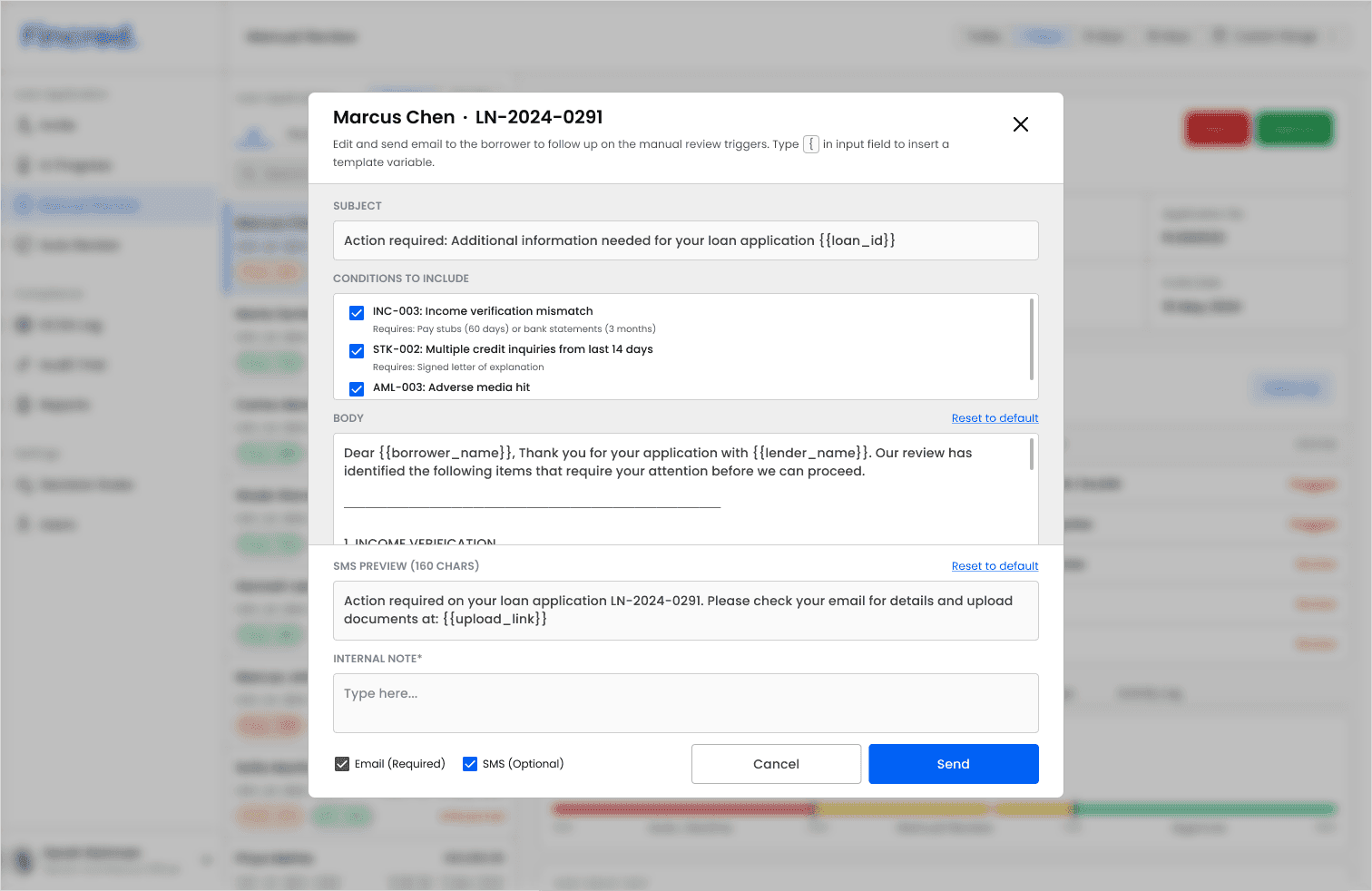

Solution: One email, all conditions within it, each pre-written for the specific check that triggered it and editable by the officer before sending. The borrower receives one clear communication: what is wrong, what is needed, and where to upload it. On the officer's side, every request is tied to the exact trigger that caused it and logged as part of the compliance record. The officer can also choose to send an SMS alongside, not a copy of the email, but a single line nudge telling the borrower to check their inbox. One send event. One audit trail entry. The application moves forward instead of stalling.

More Projects

UI / UX Design

Regulated Pre-IPO Exchange Platform - 30% Faster Trade Execution, 3x Higher Closure Rate

Rebuilding the UX architecture and trade flow system for a pre-IPO share exchange platform, from a broken, document-heavy process to a structured, automated sequence that closes more deals, faster.

UI / UX Design

Email Marketing Analytics -Turning Campaign Data into Capital-Raising Intelligence

Private token issuers were running email campaigns with no way to isolate whether underperformance was a content problem, an infrastructure problem, or an audience problem. This tool was built to answer that question precisely.

UI / UX Design

Loan Review Dashboard - designing the compliance workspace for consumer lending platforms

A compliance review dashboard consolidating identity, credit, fraud, and AML signals into one structured workspace that is designed for loan officers at regulated fintech lending platforms.

Year :

2023

Industry :

Fintech

Company

Compliance Innovation

Project Duration :

4 Months

OverView

Loan officers at consumer lending platforms make dozens of approve or reject decisions every day. Behind each decision is a completed application with outputs from identity verification, credit bureau, income verification, AML screening, and device fraud detection - separate systems, different formats, different compliance implications.

The real risk is not inefficiency. It is a missed fraud signal. On an unsecured personal loan, there is no collateral. A wrong approval is a written-off loan.

This project was to design the compliance review workspace from the ground up. A white-label platform lending companies deploy under their own brand, built to surface every verification signal in one structured interface, with actions tied directly to what triggered them, and a documented record of every decision made.

Outcome

Designed a compliance review workspace that gives loan officers complete visibility into every verification signal - identity, credit report, income, fraud, and AML, in a single structured interface. An officer can move from application received to decision made without leaving the screen or switching tools.

Fraud signals that previously required manual cross-referencing across systems are now surfaced at the point of review, tied directly to the action needed to resolve them. A wrong approval on an unsecured personal loan has no recovery path. The design makes the right call harder to miss.

My Role

End-to-end product design, user research, information architecture, interaction design, and final UI. Collaborated with the product team on compliance requirements and lending workflow validation.

Problem

Every signal is there. The system to act on them isn't.

Loan officers need to make accurate credit decisions at speed but the data required to make that decision is spread across identity, credit, income, fraud, and AML systems with no unified view and no hierarchy telling them what matters most.

Fragmented verification data increases cognitive load at the exact moment it needs to be lowest. An officer processing disconnected signals manually is more likely to miss the connection between them. And on an unsecured loan, a missed fraud signal has no recovery path.

Not every flagged application is a rejection. Many are recoverable with one document or one clarification. Without a structured follow-up workflow, those borrowers are lost not because of the risk they posed but because the process had no way to bring them back.

Solution

Iteration 1

The first version was the obvious one. Every verification output in one place, identity, credit, income, fraud, AML, unified in a single interface. Technically complete. A loan officer could see everything without switching tools.

Final Design

But seeing everything is not the same as knowing what matters. The officer was still doing the interpretive work manually, scanning a full list to find the three signals worth acting on. The interface had consolidated the data. It had not supported the decision.

That forced the real design question. An officer reviewing a loan application is not reading a report. They are looking for a pattern, a signal that one check alone might not confirm but two or three together do. The interface needed to reflect that. Surface what requires attention. Let the officer investigate the rest if they choose.

That shift changed the structure of the entire product. The review area became focused on triggered signals only. Full verification data remained accessible but was no longer the primary view. The officer lands on what matters, not on what exists.

Follow up with borrower feature

Not every flagged application is a rejection. Many just need one document or one clarification from the borrower. Without a structured way to ask, those applications quietly die.

Solution: One email, all conditions within it, each pre-written for the specific check that triggered it and editable by the officer before sending. The borrower receives one clear communication: what is wrong, what is needed, and where to upload it. On the officer's side, every request is tied to the exact trigger that caused it and logged as part of the compliance record. The officer can also choose to send an SMS alongside, not a copy of the email, but a single line nudge telling the borrower to check their inbox. One send event. One audit trail entry. The application moves forward instead of stalling.

More Projects

UI / UX Design

Regulated Pre-IPO Exchange Platform - 30% Faster Trade Execution, 3x Higher Closure Rate

Rebuilding the UX architecture and trade flow system for a pre-IPO share exchange platform, from a broken, document-heavy process to a structured, automated sequence that closes more deals, faster.

UI / UX Design

Email Marketing Analytics -Turning Campaign Data into Capital-Raising Intelligence

Private token issuers were running email campaigns with no way to isolate whether underperformance was a content problem, an infrastructure problem, or an audience problem. This tool was built to answer that question precisely.

UI / UX Design

Loan Review Dashboard - designing the compliance workspace for consumer lending platforms

A compliance review dashboard consolidating identity, credit, fraud, and AML signals into one structured workspace that is designed for loan officers at regulated fintech lending platforms.

Year :

2023

Industry :

Fintech

Company

Compliance Innovation

Project Duration :

4 Months

OverView

Loan officers at consumer lending platforms make dozens of approve or reject decisions every day. Behind each decision is a completed application with outputs from identity verification, credit bureau, income verification, AML screening, and device fraud detection - separate systems, different formats, different compliance implications.

The real risk is not inefficiency. It is a missed fraud signal. On an unsecured personal loan, there is no collateral. A wrong approval is a written-off loan.

This project was to design the compliance review workspace from the ground up. A white-label platform lending companies deploy under their own brand, built to surface every verification signal in one structured interface, with actions tied directly to what triggered them, and a documented record of every decision made.

Outcome

Designed a compliance review workspace that gives loan officers complete visibility into every verification signal - identity, credit report, income, fraud, and AML, in a single structured interface. An officer can move from application received to decision made without leaving the screen or switching tools.

Fraud signals that previously required manual cross-referencing across systems are now surfaced at the point of review, tied directly to the action needed to resolve them. A wrong approval on an unsecured personal loan has no recovery path. The design makes the right call harder to miss.

My Role

End-to-end product design, user research, information architecture, interaction design, and final UI. Collaborated with the product team on compliance requirements and lending workflow validation.

Problem

Every signal is there. The system to act on them isn't.

Loan officers need to make accurate credit decisions at speed but the data required to make that decision is spread across identity, credit, income, fraud, and AML systems with no unified view and no hierarchy telling them what matters most.

Fragmented verification data increases cognitive load at the exact moment it needs to be lowest. An officer processing disconnected signals manually is more likely to miss the connection between them. And on an unsecured loan, a missed fraud signal has no recovery path.

Not every flagged application is a rejection. Many are recoverable with one document or one clarification. Without a structured follow-up workflow, those borrowers are lost not because of the risk they posed but because the process had no way to bring them back.

Solution

Iteration 1

The first version was the obvious one. Every verification output in one place, identity, credit, income, fraud, AML, unified in a single interface. Technically complete. A loan officer could see everything without switching tools.

Final Design

But seeing everything is not the same as knowing what matters. The officer was still doing the interpretive work manually, scanning a full list to find the three signals worth acting on. The interface had consolidated the data. It had not supported the decision.

That forced the real design question. An officer reviewing a loan application is not reading a report. They are looking for a pattern, a signal that one check alone might not confirm but two or three together do. The interface needed to reflect that. Surface what requires attention. Let the officer investigate the rest if they choose.

That shift changed the structure of the entire product. The review area became focused on triggered signals only. Full verification data remained accessible but was no longer the primary view. The officer lands on what matters, not on what exists.

Follow up with borrower feature

Not every flagged application is a rejection. Many just need one document or one clarification from the borrower. Without a structured way to ask, those applications quietly die.

Solution: One email, all conditions within it, each pre-written for the specific check that triggered it and editable by the officer before sending. The borrower receives one clear communication: what is wrong, what is needed, and where to upload it. On the officer's side, every request is tied to the exact trigger that caused it and logged as part of the compliance record. The officer can also choose to send an SMS alongside, not a copy of the email, but a single line nudge telling the borrower to check their inbox. One send event. One audit trail entry. The application moves forward instead of stalling.

More Projects

UI / UX Design

Regulated Pre-IPO Exchange Platform - 30% Faster Trade Execution, 3x Higher Closure Rate

Rebuilding the UX architecture and trade flow system for a pre-IPO share exchange platform, from a broken, document-heavy process to a structured, automated sequence that closes more deals, faster.

UI / UX Design

Email Marketing Analytics -Turning Campaign Data into Capital-Raising Intelligence

Private token issuers were running email campaigns with no way to isolate whether underperformance was a content problem, an infrastructure problem, or an audience problem. This tool was built to answer that question precisely.